Your Home Closing Timeline In London

January 1, 2026

January 1, 2026

You found the right home in London and your offer was accepted. Now what? The time between yes and keys can feel fuzzy, especially if you are a first-time buyer or relocating to Madison County. You want clear steps, realistic timing, and a smooth path to closing.

This guide breaks down each stage from contract to closing, explains typical Central Ohio timelines, and flags local items that can add time around London. You will also get simple checklists and common delay busters so you can stay on track. Let’s dive in.

After acceptance, you and the seller sign the purchase agreement and open the file with the title company and your lender. You typically deposit earnest money within 1 to 5 business days based on your contract. Prompt delivery of all documents helps the entire timeline.

The title company orders a title search and issues a title commitment. This checks for liens, judgments, easements, taxes, and other items that must be cleared before closing. In Central Ohio, a preliminary title commitment often arrives in 3 to 10 business days, but older properties or complex histories can take longer.

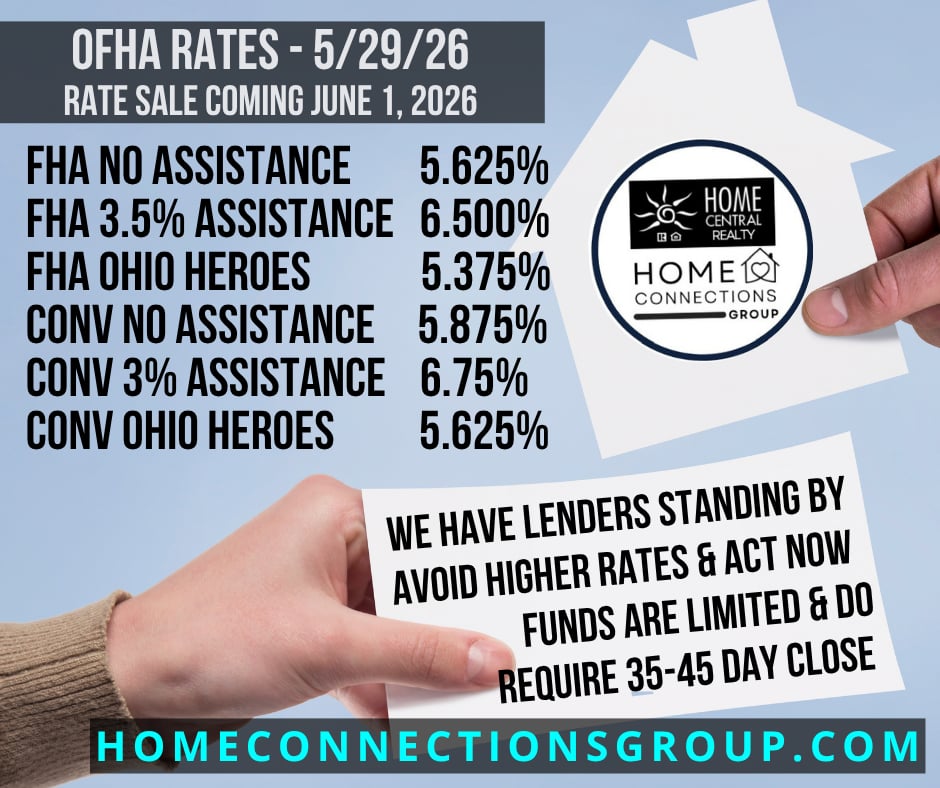

You submit your loan application and initial documents. These commonly include ID, income and asset statements, tax returns, and proof of homeowner’s insurance. Your lender orders the appraisal soon after application.

You schedule a general home inspection and any specialized inspections you choose. Around London, buyers often add pest, radon, sewer scopes, and for rural homes, well water testing and septic inspections. Negotiations on repairs or credits typically take 1 to 2 weeks depending on findings and contractor schedules.

Appraisals usually return within 7 to 14 days after they are ordered, sometimes longer for FHA, VA, or rural properties. Underwriting reviews the file and issues conditions that must be cleared for final approval. Combined appraisal and underwriting often take 14 to 30 days for conventional loans, and 30 to 45 or more for FHA, VA, or USDA.

While financing progresses, the title company clears any title exceptions. They obtain payoff statements for the seller’s mortgages and collect HOA documents if needed. Payoffs and HOA paperwork can take several days to two weeks.

Once conditions are met, the lender issues clear to close and coordinates the closing date with the title company. By federal rule, the lender must provide the Closing Disclosure at least 3 business days before closing. Build this timing into your expectations.

You complete a final walkthrough within 24 hours of closing to confirm the home’s condition and any agreed repairs. At the appointment, you sign documents, present a certified check or send a bank wire for closing funds, and the title company finalizes the settlement. Keys are released after funds are confirmed and documents are recorded.

The deed and mortgage are recorded with the Madison County Recorder. Many transactions fund and record the same day. If recording or funding is delayed, keys are delivered once the title company confirms both steps are complete.

Remember, the Closing Disclosure must be delivered at least 3 business days before you sign. This rule often sets the earliest possible closing date.

Many homes outside London’s city utilities rely on private wells and septic systems. Water tests and septic inspections are common buyer contingencies and may be required by some loan programs. If repairs or permitting are needed, plan for extra days.

Title work can surface agricultural easements, conservation restrictions, survey questions, or fencing boundary issues. Address these early to avoid last-minute title delays. Some rural properties may qualify for USDA loans, which can add time for appraisal and program review.

In Ohio, closings are often conducted by title companies, and attorneys may also handle them. Local custom varies, so ask what is typical in Madison County when you go under contract.

In many Central Ohio transactions, sellers often pay for the owner’s title policy and buyers pay for the lender’s policy. This is a custom and can be negotiated in your contract. Your agent and title company will confirm the norm for your specific deal.

Recording occurs at the county level through the Madison County Recorder. Real estate taxes are prorated at closing based on the schedule set by the Madison County Auditor and Treasurer. Any tax delinquencies or special assessments must be addressed before closing.

Plan for 60 to 90 minutes to sign documents, review the settlement statement, and complete funding. You will either provide a certified check or send a bank wire per instructions from the title company. Once the deed and mortgage are recorded and funds are disbursed, you receive keys and can start your move.

If you want a calm, organized path from accepted offer to keys, our team brings step-by-step guidance and proven systems to every closing. Whether you are buying your first home or relocating to Central Ohio, we coordinate the details so you can focus on your move. Connect with Home Connections Group - Home Central Realty. Let's Get You Home.

Real Estate

Lifestyle

Franklin Park Conservatory

We are with you from the beginning of the process through your closing, providing full service and expertise every step of the way.

1156 DUBLIN ROAD, SUITE 105 COLUMBUS, OH 43215